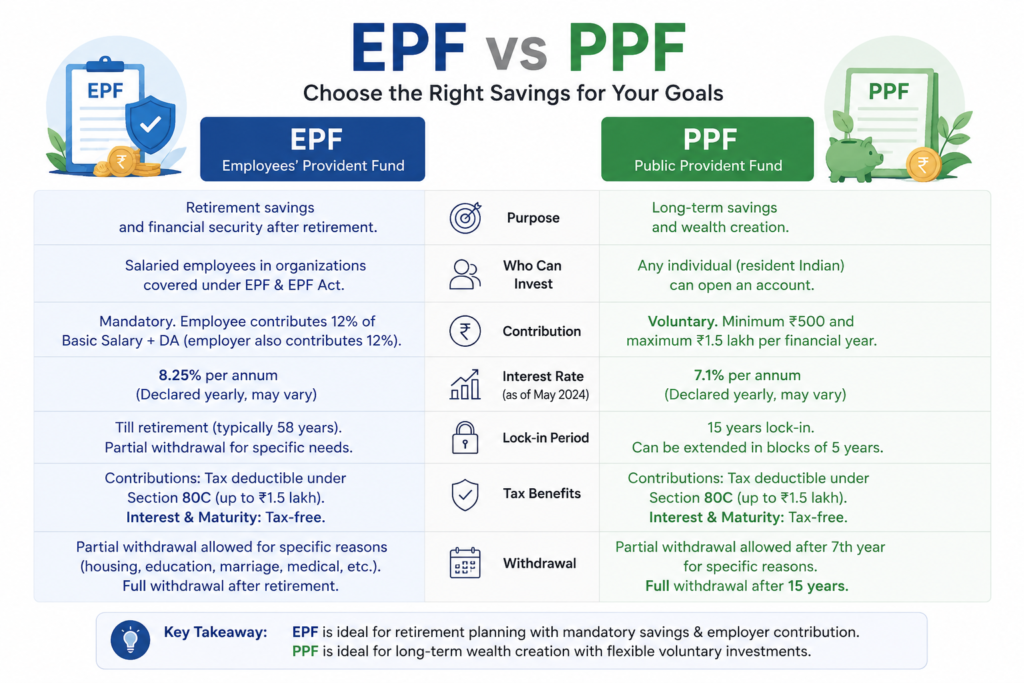

When planning for long-term financial security, many investors compare EPF vs PPF to determine which option best suits their retirement and savings goals. Both the Employees’ Provident Fund (EPF) and the Public Provident Fund (PPF) are government-backed investment schemes that offer attractive interest rates and tax benefits. However, they differ in eligibility, contribution structure, lock-in period, and withdrawal rules. Understanding the EPF vs PPF comparison can help you make an informed financial decision.

What is EPF?

The Employees’ Provident Fund (EPF) is a retirement savings scheme for salaried employees working in organizations covered under the EPF Act. Both the employee and employer contribute a fixed percentage of the employee’s basic salary and dearness allowance every month. The accumulated amount earns annual interest declared by the government and becomes a valuable retirement corpus.

EPF offers disciplined savings because contributions are deducted directly from the employee’s salary. Partial withdrawals are allowed under specific conditions such as buying a house, medical emergencies, higher education, or marriage.

What is PPF?

The Public Provident Fund (PPF) is a long-term savings scheme available to all Indian residents, including self-employed individuals and those without employer-sponsored retirement benefits. Investors can open a PPF account in banks or post offices and contribute between the prescribed annual minimum and maximum limits.

PPF has a 15-year lock-in period, making it an excellent option for long-term financial planning. The account also allows partial withdrawals and loan facilities after completing the required eligibility period.

Key Differences Between EPF and PPF

One of the biggest differences is eligibility. EPF is mainly for salaried employees, while PPF is open to almost every Indian resident.

Another difference is contribution. EPF contributions are salary-based and shared by both the employee and employer. In contrast, PPF contributions are voluntary and made entirely by the account holder.

Liquidity also differs. EPF allows withdrawals under certain conditions before retirement, whereas PPF has a longer lock-in period with limited withdrawal options.

Both schemes enjoy tax benefits under the applicable provisions of the Income Tax Act and generally offer tax-free interest and maturity benefits, subject to prevailing tax rules.

Which One Should You Choose?

If you are a salaried employee, EPF should usually be your primary retirement savings tool because of the employer’s contribution, which significantly increases your retirement corpus.

PPF is an excellent choice for self-employed individuals, freelancers, business owners, or salaried employees who want to diversify their retirement savings beyond EPF. Its government backing and guaranteed returns make it a reliable investment for conservative investors.

Many financial planners recommend investing in both EPF and PPF whenever possible. This combination provides diversification, stable returns, and additional retirement security.

Final Thoughts

Choosing between EPF and PPF depends on your employment status, financial goals, and investment strategy. EPF provides automatic retirement savings with employer support, while PPF offers flexibility and accessibility for everyone seeking long-term wealth creation.

Instead of viewing EPF and PPF as competing investment options, consider how they can complement each other in your financial plan. By investing consistently and staying committed to your long-term goals, you can build a strong financial foundation and enjoy greater peace of mind during retirement.